Chapter 7 vs. Chapter 13 in Seattle: Which Bankruptcy Is Right for You?

If you are struggling with debt in Seattle, you may be wondering whether Chapter 7 or Chapter 13 bankruptcy is the best choice for your situation. Both options are designed to provide financial relief, but they work in very different ways. Understanding the differences can help you make the right decision for your finances and future.

What Is the Difference Between Chapter 7 and Chapter 13?

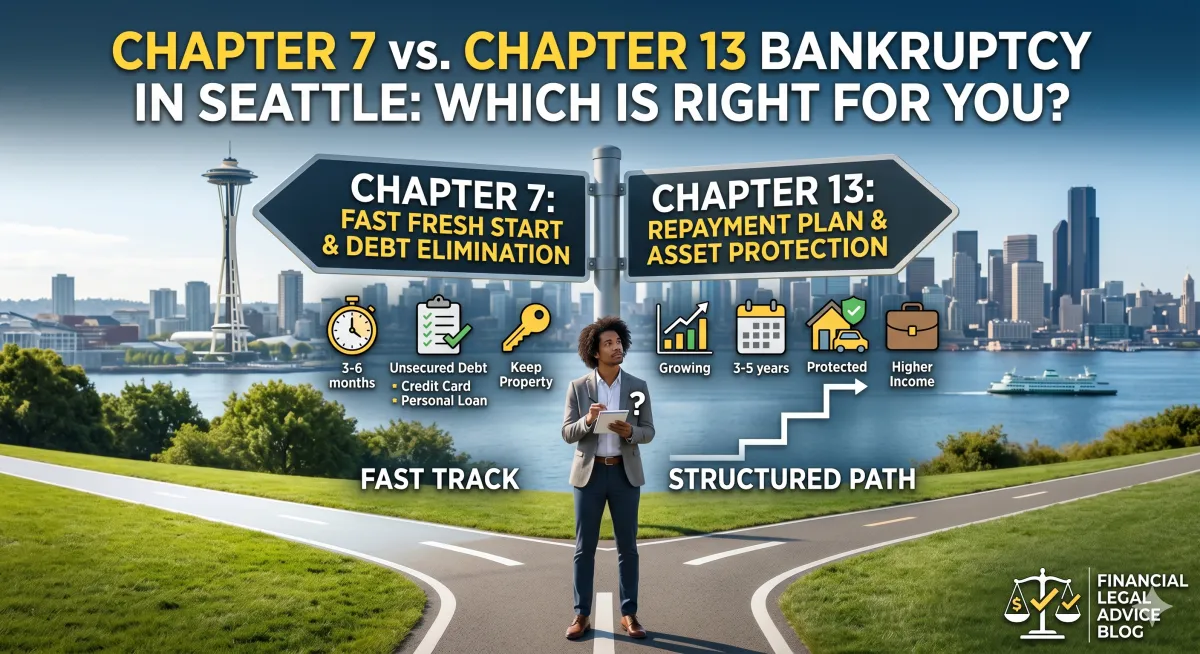

Chapter 7 bankruptcy is often called “liquidation bankruptcy.” It allows individuals to eliminate most unsecured debts, such as credit cards and personal loans, typically within a few months. In most cases, you can keep essential assets thanks to Washington State exemptions. Chapter 7 provides a relatively fast fresh start for those who qualify.

Chapter 13 bankruptcy, on the other hand, is known as a “reorganization bankruptcy.” Instead of discharging debts outright, it establishes a repayment plan over three to five years. Chapter 13 is particularly useful for individuals with higher income, significant non-exempt property, or debts they can repay gradually but need legal protection to do so.

The core difference is simple: Chapter 7 eliminates debt quickly, while Chapter 13 allows you to repay it over time under court supervision.

Key Factors to Consider When Choosing

When deciding between Chapter 7 and Chapter 13, several factors come into play:

Income level and eligibility: Chapter 7 requires passing the means test, while Chapter 13 is available to higher-income individuals.

Ability to repay debts: Chapter 13 is ideal for those who can afford monthly payments but need structure to do so.

Type of debt owed: Some debts, like certain tax obligations or secured debts, may be easier to manage under Chapter 13.

Financial goals: Chapter 7 offers faster relief, whereas Chapter 13 may help protect property and manage larger repayment obligations.

Each factor should be weighed carefully to determine which bankruptcy type aligns with your circumstances.

Which Option May Be Right for You?

For many individuals with low income and mostly unsecured debts, Chapter 7 is often the preferred choice. It offers a quicker discharge of debts and a clean start without a long repayment plan.

Chapter 13 may be the better fit if you have significant assets you want to protect, consistent income to make monthly payments, or debts that cannot be discharged in Chapter 7, such as certain tax obligations or recent loans.

Ultimately, the right choice depends on your unique financial situation. Reviewing your income, debts, and long-term goals is critical before moving forward.

Take the Next Step

There is no one-size-fits-all solution when it comes to bankruptcy. Understanding the differences between Chapter 7 and Chapter 13 is the first step in making an informed decision.

Schedule a consultation today to determine which bankruptcy option is right for you in Seattle and take control of your financial future.